This article is adapted from the downloadable guide in slide format. We suggest downloading the slides via the "Download Article PDF" button in the upper right.

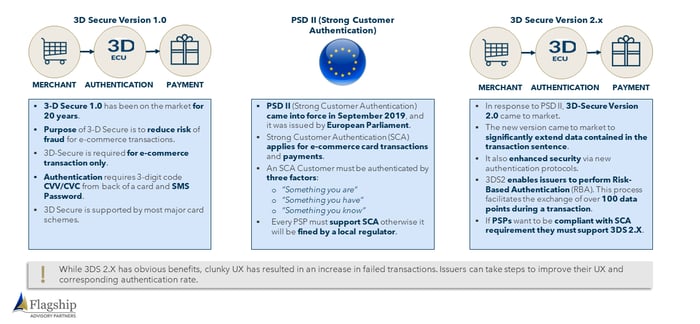

3D Secure has been on the market for some time, but PSD II regulation brought significant updates which provide optionality for issuers.

FIGURE 1: Summary of 3D Secure

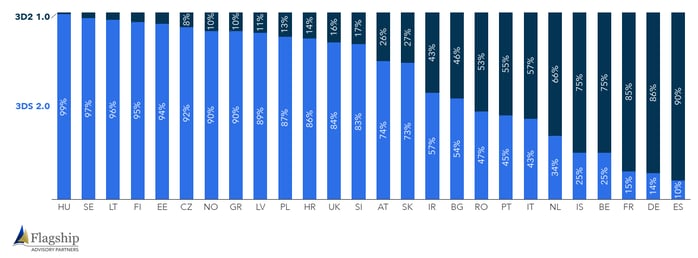

FIGURE 2: Transactions Using 3D Secure Version 1.0 & 2.x (2022; % of transactions)

Source: Ravelin PSD2 and global payment regulation map 2022

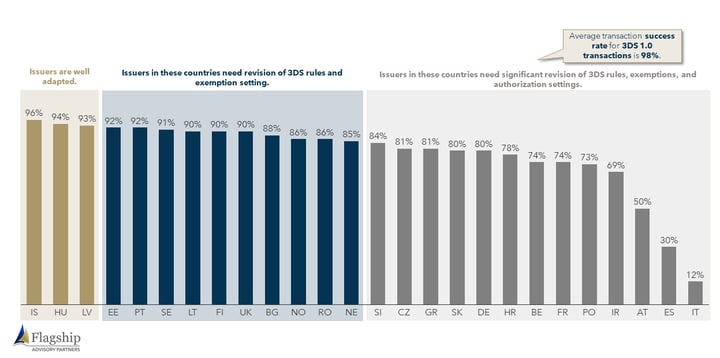

FIGURE 3: Authentication Success Rate by European Country (2022; % of 3DS 2.x transactions)

Source: Ravelin PSD2 and global payment regulation map 2022

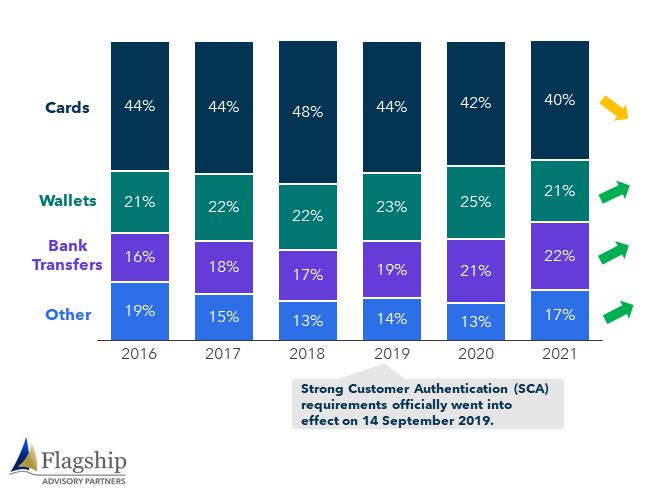

SCA requirements can partially help explain some observed downturns in card usage online between 2019 and 2020.

FIGURE 4: Online EU Payment Tool Usage (weighted average, in %)

Note: Other consists of Invoice payments, Cash-based payments. Weighted Average Payment Tools consists of Belgium, Denmark, France, Germany, Italy, Netherlands, Norway, Poland, Spain, Sweden, UK.

Source: Global Data Survey

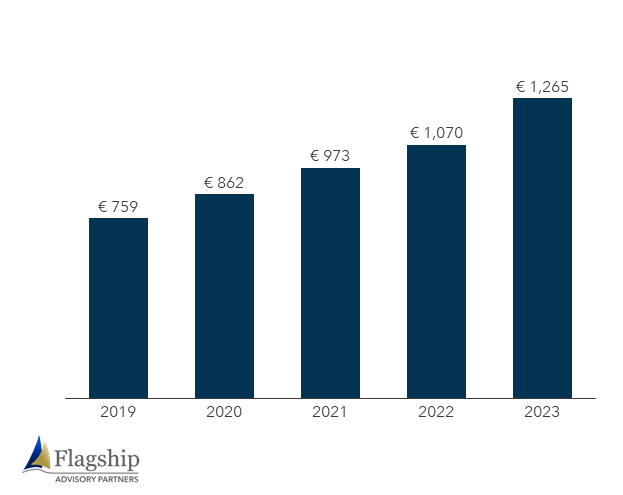

FIGURE 5: Total EU e-Commerce Turnover (2016-2020; in € mil.)

Source: Global Data Survey

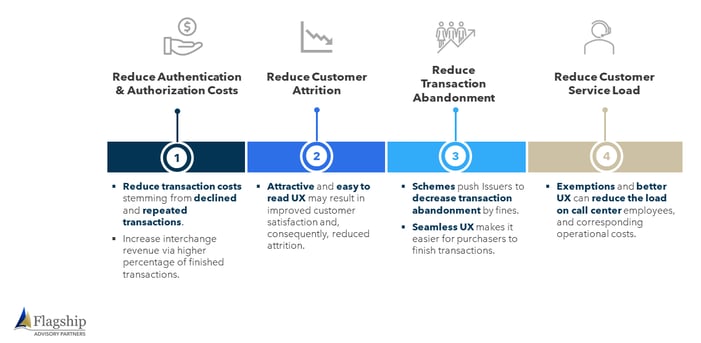

Issuers can significantly reduce abandonment and boost e-commerce volume by setting up SCA and UX properly.

FIGURE 6: Issuers and Acquirers Benefits from Proper Setting of 3D Secure Rules

Source: Flagship Advisory Partners

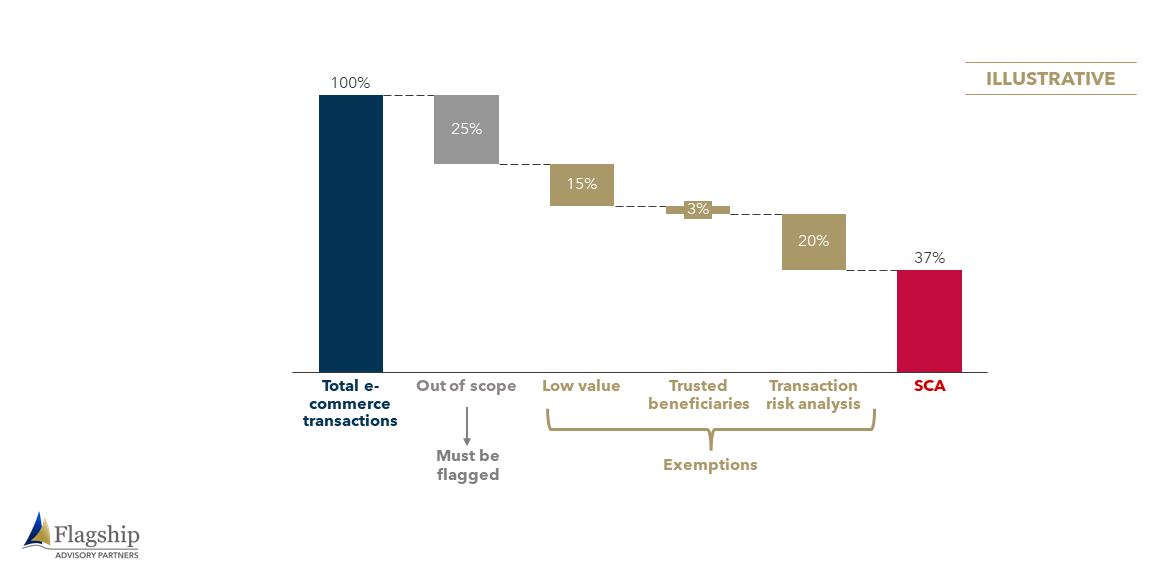

Issuers can drastically reduce the number of SCA-required transactions by setting up detection of out-of-scope transactions and by using exemptions.

FIGURE 7: Illustrative Moderately-Optimistic Scenario of % of Transactions Requiring SCA

Source: Visa, Flagship Advisory Partners analysis

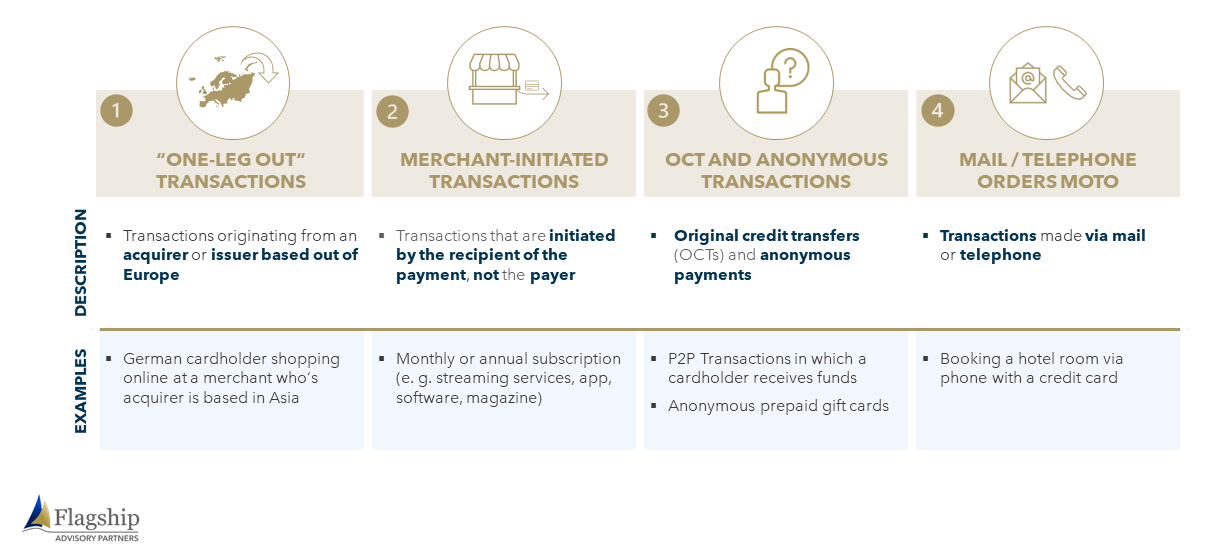

The first step to improving UX is to identify out-of-scope transactions and decrease the rate of failed or abandoned transactions.

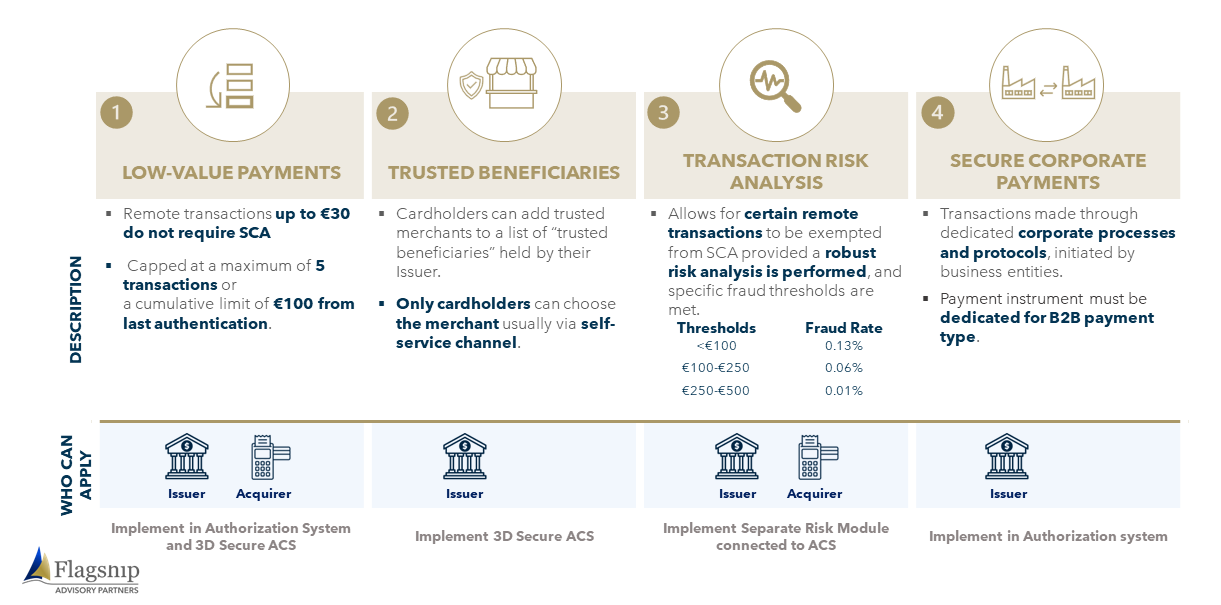

FIGURE 8: Out of Scope Transaction Types

Source: Flagship Advisory Partners

After flagging out-of-scope transactions, the second step to improving 3DS UX is to determine 3DS exemption protocols.

FIGURE 9: Exemptions for Strong Customer Authentication

Source: Flagship Advisory Partners

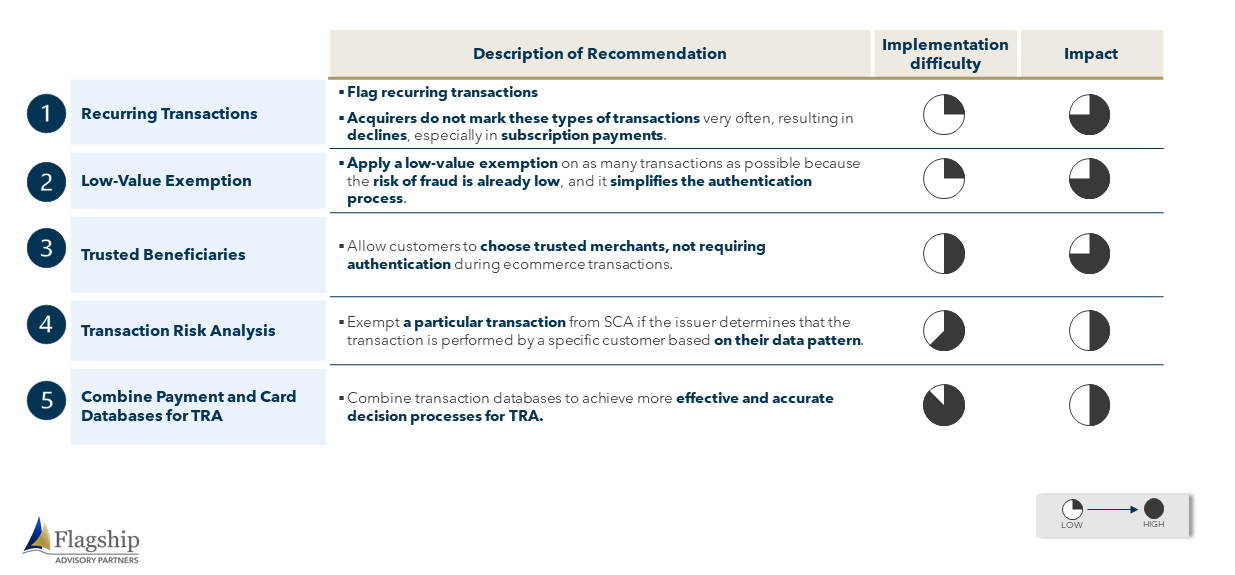

Issuers should invest in 3DS UX to improve the authentication process for customers.

FIGURE 10: Summary of Recommendations for Better 3DS UX

Source: Flagship Advisory Partners

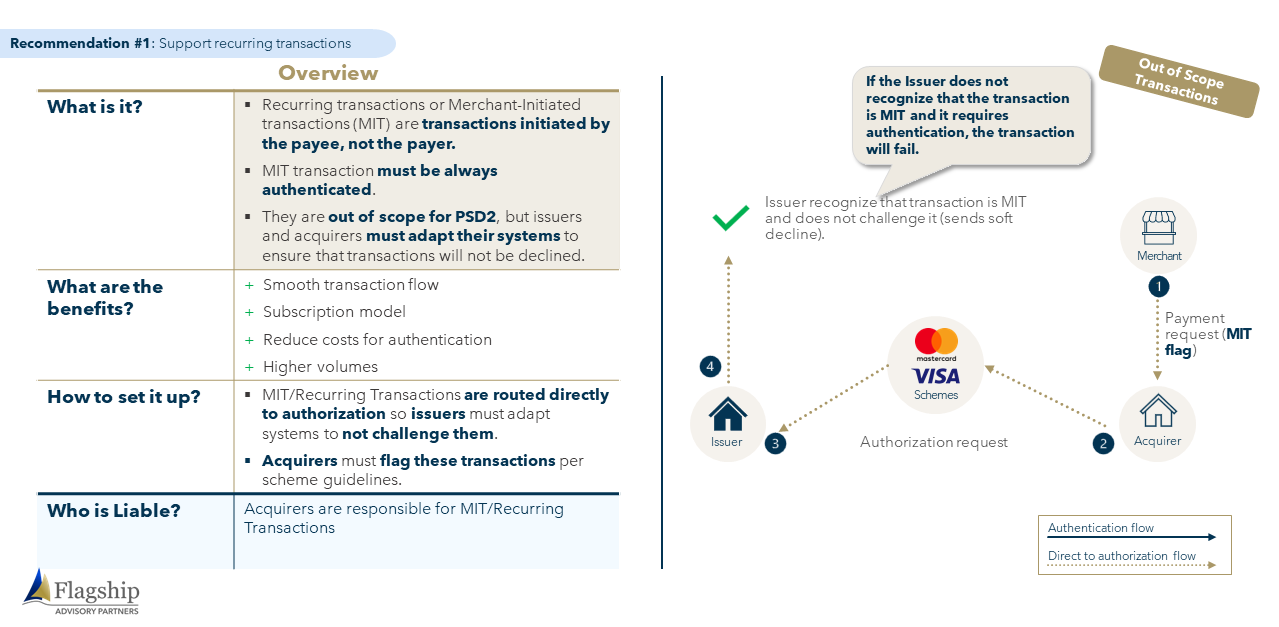

Recurring transactions are out of PSD2 scope, but issuers and acquirers need to adapt their systems to support these types of transactions, otherwise all of them will fail.

FIGURE 11: Recommendation #1 - Support Recurring Transactions

Source: Flagship Advisory Partners

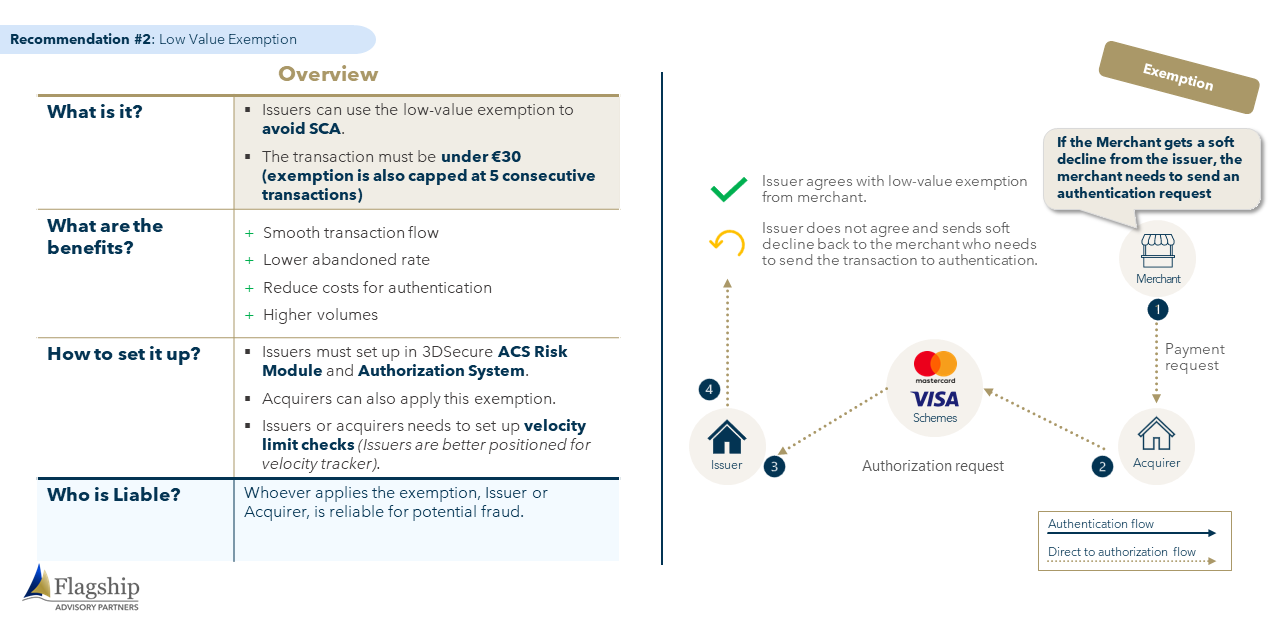

Issuers and acquirers can exempt ‘Low Value Transactions’ <€30. Issuers are better positioned for this type of exemption as they have a velocity limit tracker.

FIGURE 12: Recommendation #2 - Low Value Exemption

Source: Flagship Advisory Partners

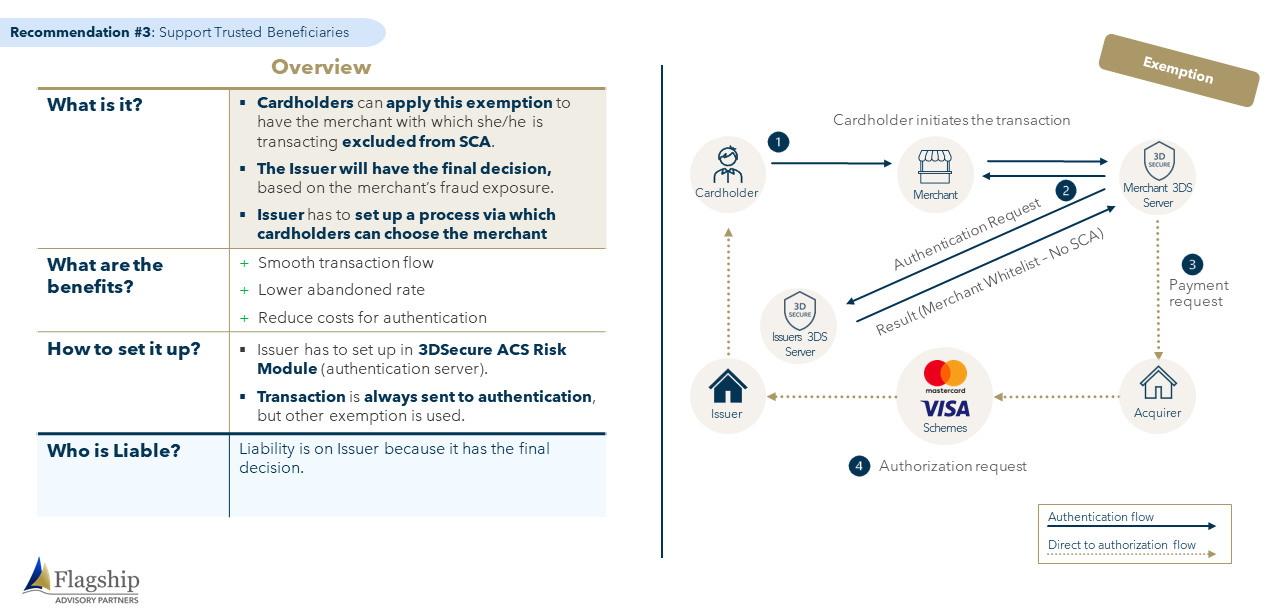

Only Issuers can apply trusted beneficiary exemptions based on fraud exposure. It is an easy, effective, and safe exemption which will ensure a higher approval rate and reduce the authentication costs.

FIGURE 13: Recommendation #3 - Support Trusted Beneficiaries

Source: Flagship Advisory Partners

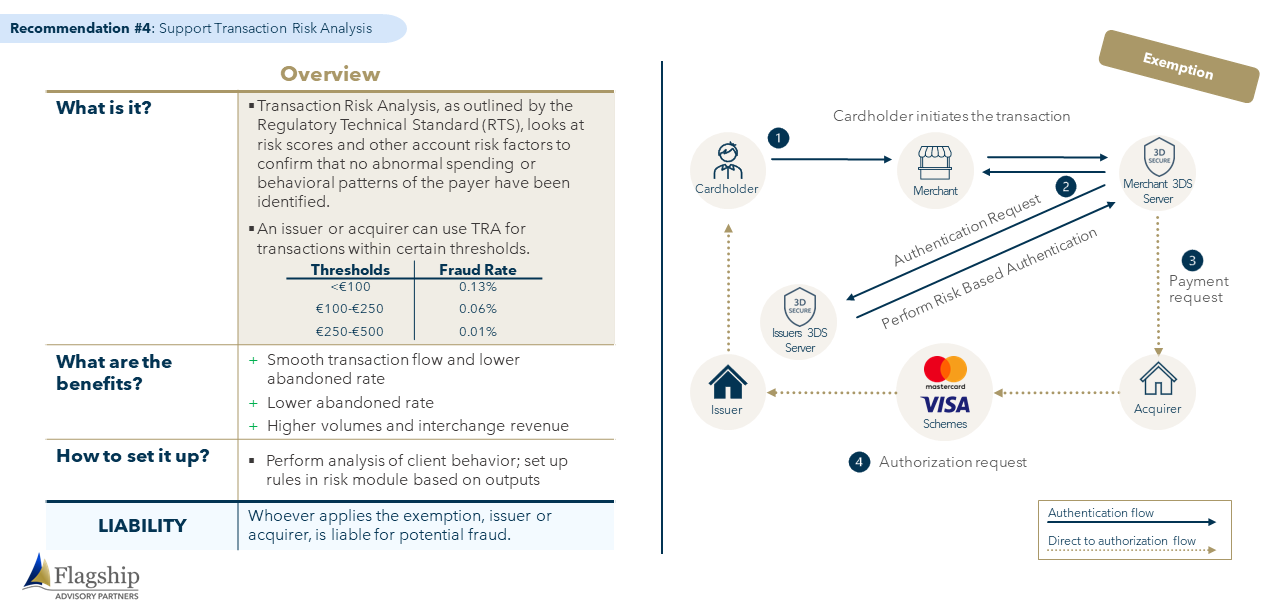

Rules for transaction risk analysis are difficult to set up and require long-term analysis, but can significantly decrease abandonment and improve the customer experience.

FIGURE 14: Recommendation #4 - Support Transaction Risk Analysis

Source: Flagship Advisory Partners

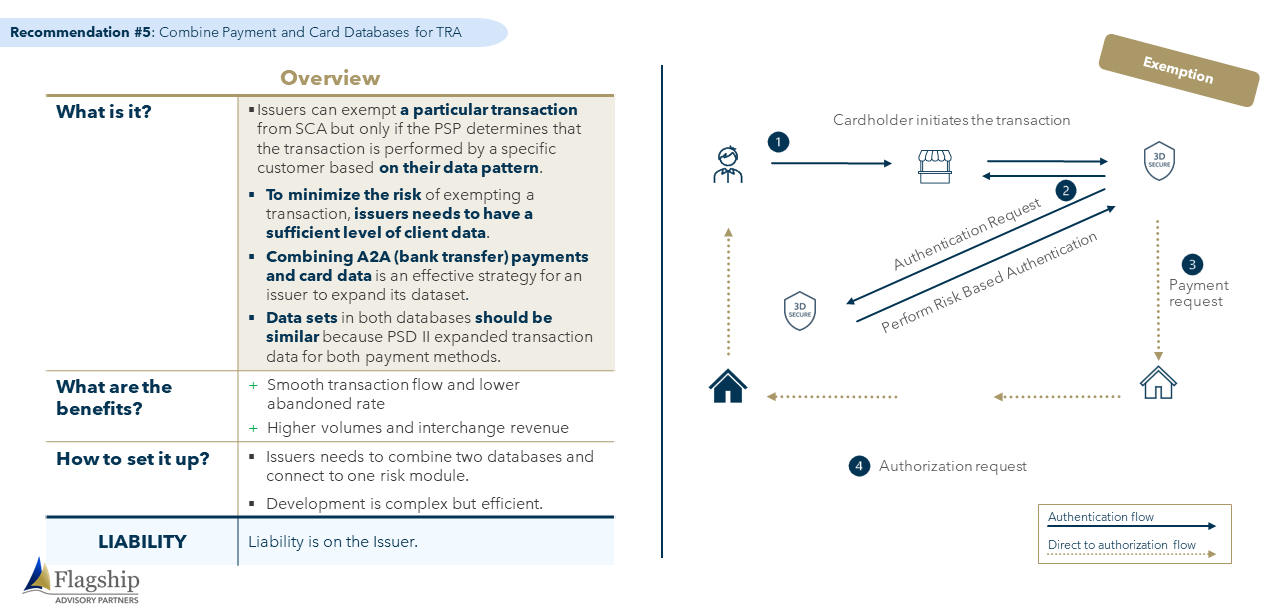

Transaction Risk Analysis is an efficient tool to save authentication cost and avoid the need for SCA. With more data, issuers can improve decisioning.

FIGURE 15: Recommendation #5 - Combine Payment and Card Databases for TRA

Source: Flagship Advisory Partners

Please do not hesitate to contact Erik Howell at Erik@FlagshipAP.com or Stanislav Dubsky at Stanislav@FlagshipAP.com with comments or questions.