The fintech equity markets, public and private, have been sellers’ markets for years. Particularly during the pandemic, the premium placed on high growth fintechs reached stratospheric levels. Those days could be ending.

The sunset of the pandemic, rise of inflation, and war in Ukraine have public investors shifting towards alternative asset classes and away from tech and high-growth equities. Hedge funds that piled into fintech and software growing during the pandemic were recently shorting these same equities (though these shorts appear to be unwinding quickly this week).

Absent a dramatic turnaround in the coming weeks, we anticipate a wave of public to private equity transactions in the remainder of 2022. Several high-profile fintech IPOs, most notably Stripe, were on the horizon for 2022, but now may be postponed.

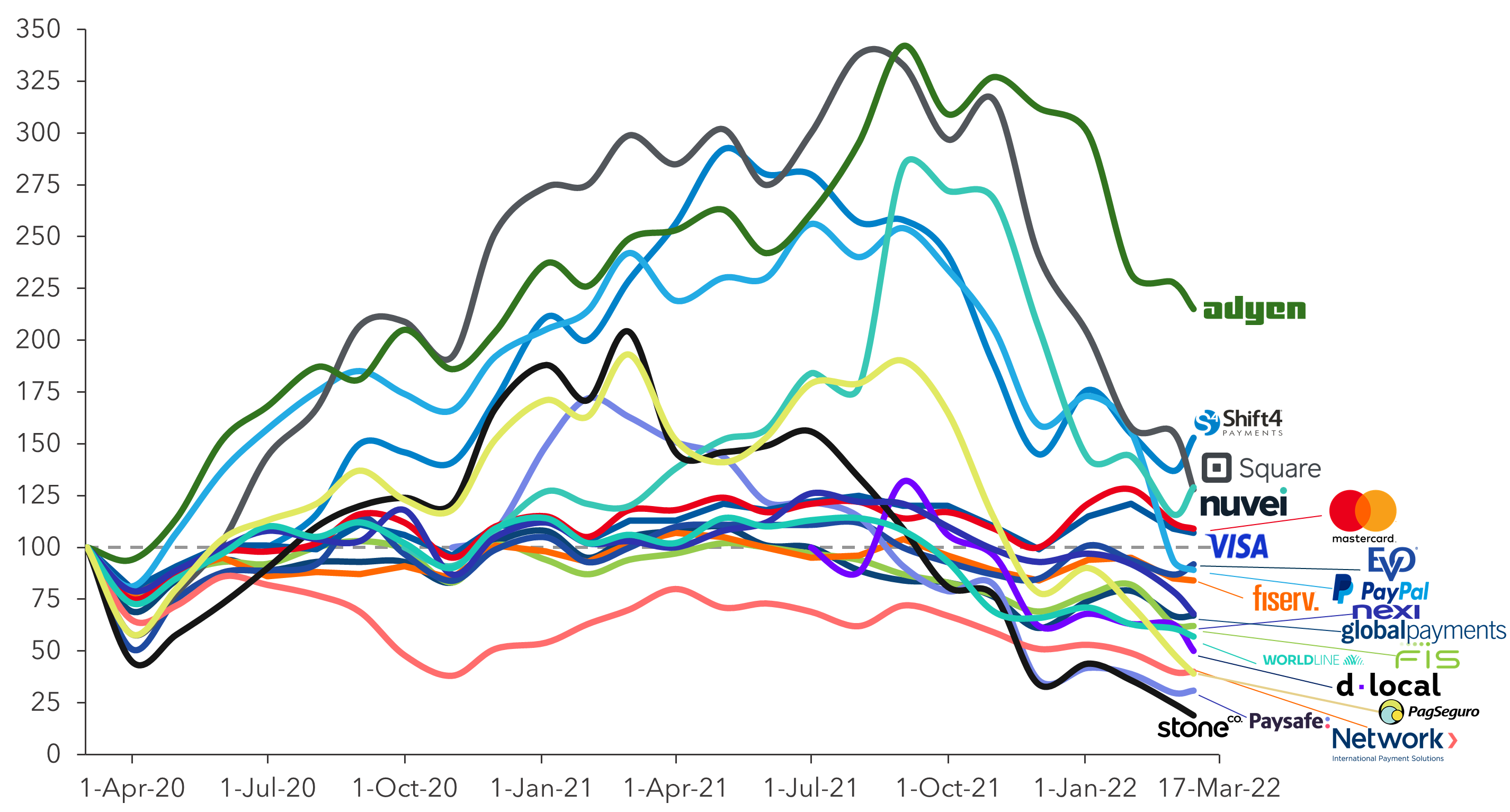

FIGURE 1: Share Performance of Select Fintech Public Equities (indexed to 100 from 2 March 2020; based on closing 17 March 2022)

Source: Flagship Advisory Partners, Yahoo Finance

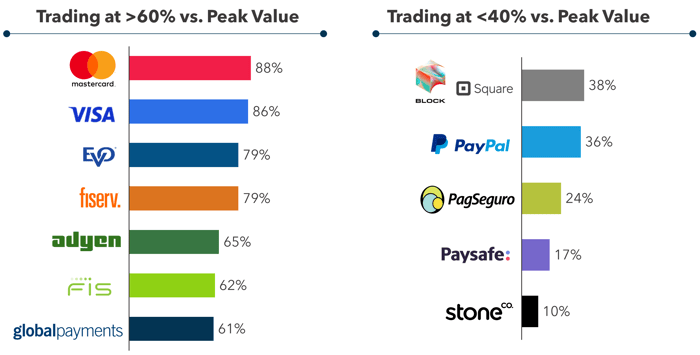

While there has clearly been a valuation crunch, many fintech public equities are far from cheap (Adyen still trades at 73x trailing EBITDA). What has emerged is a separation of the pack, to some extent, between companies that have retained value (<40% reduction in share price from peak to today) and companies being punished under current market conditions (>60% reduction in share price from peak to today). As shown in Figure 2, Fintechs that have retained value are generally those that are highly cash generative and less likely to be valued based on lofty growth expectations.

FIGURE 2: Current Trading vs Peak Value of Select Fintech Public Equities (select examples; based on closing 17 March 2022)

Source: Flagship Advisory Partners, Yahoo Finance

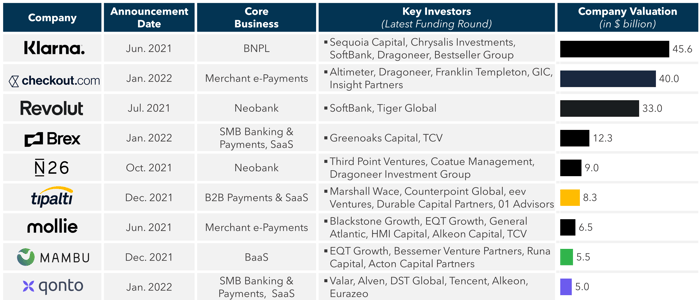

We are starting to see the impacts of public valuation pressure also in the private equity and M&A markets, and we expect an acceleration of this pressure if public valuations remain as is. As shown in Figure 3, growth private equity funding activity has been exceptional in the last two years, often at valuations of 30-60x revenue. Klarna was last funded at 28x 2021 operating income, Brex at an estimated 38x 2021 revenue, and Revolut at an estimated 50-60x est. 2021 revenue. By comparison, in the public equity markets, Block (Square) now trades at 3.2x 2021 gross revenue and 12.8x 2021 gross profit and Adyen trades at 7.6x gross revenue and 46x gross profit.

FIGURE 3: Select, Recent, Fintech Private Growth Equity Funding Rounds

Source: Flagship Advisory Partners, press releases

Source: Flagship Advisory Partners, press releases

These types of valuations are supported, in part, by expectations for future IPO values. As public market valuations recalibrate (which certainly seems to be the case at present), valuations on private equity will similarly decline. There remain massive amounts of private capital in search of returns, so we do not foresee a major drop-off in deal activity. However, we do expect both venture and growth equity investors to focus more on cashflow generation fundamentals and seeing a clearer path to EBITDA positive, not just topline growth ad infinitum.

Please do not hesitate to contact Joel Van Arsdale at Joel@FlagshipAP.com with comments or questions.