Aigerim Assembayeva, Pedro Giesta, and Maxim van Hoorn • 14 April, 2023

Infographic: LatAm Fintech Landscape, 2023

General Observations

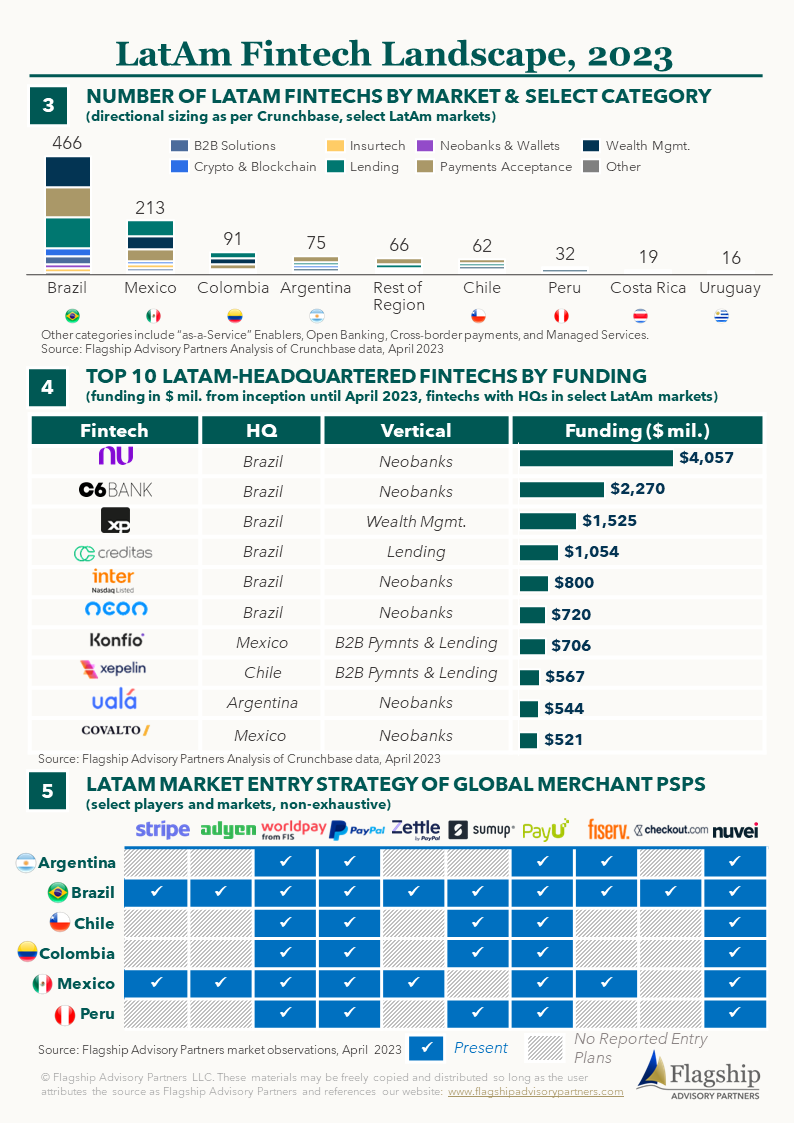

As of April 2023, there are ~1,000 active fintechs in LatAm (vs. ~3,300 in Europe and ~4,200 in the US).

~70% of all LatAm fintechs specialize in lending, payment acceptance, and wealth management & investment (similar category breakdown as the US and Europe).

~65% of LatAm fintechs are based in either Brazil or Mexico.

The LatAm payments acceptance space has been growing fast, propelled primarily by domestic players (e.g., PagSeguro, Mercado Pago, Stone, etc.) offering mPOS terminals, digital payments, and other solutions. We expect further growth to be driven by fintechs such as dLocal and Ebanx, expanding outside the LatAm region.

Global PSPs such as Stripe, Adyen, and SumUp are increasing their presence in the region, focusing on the largest markets first. Due to its sheer size, Brazil is often the first entry point for international PSPs expanding to the region (e.g., Adyen opened an office in Brazil in 2011 and SumUp in 2013)

Instant Payment Schemes

Several LatAm countries have introduced instant payment initiatives running on account-to-account rails. The largest are state-owned such as PIX (Brazil) and CoDi (Mexico); although there are also privately-owned schemes in Colombia (Transfiya) and Peru (Yape and PLIN).

The Brazilian Central Bank launched PIX in 2020, which is rapidly growing in adoption. As of 2022, PIX reached ~$200 bil. in monthly transactions and has been used by ~130 mil. users. As one of the global poster children for A2A schemes, PIX presents serious challenges to legacy and cards-based payments infrastructure.

Other LatAm instant payment initiatives haven’t gained such massive traction as PIX. Since September 2019 to March 2022, ~$316 mil. transactions were processed via Mexican CoDi by ~17 mil. registered users. Private-led real-time payments initiatives in Colombia (Transfiya with < ~2 mil. users) and Peru (Yape and PLIN, each having < ~10 mil. users) are still in the early days of development. It is worth mentioning that Peru’s Central Bank mandated Yape and PLIN to interoperate from 2023 to eliminate the friction in instant payments; as a next stage the Peruvian regulator is planning to establish a general interoperability system to connect all fintechs and banks in the country.

Despite current relative success, instant payments schemes have the potential to disrupt the lucrative cards market, driving the growth of digital payments and opening new opportunities for LatAm fintechs.

As of April 2023, there are ~1,000 active fintechs in LatAm (vs. ~3,300 in Europe and ~4,200 in the US).

~70% of all LatAm fintechs specialize in lending, payment acceptance, and wealth management & investment (similar category breakdown as the US and Europe).

~65% of LatAm fintechs are based in either Brazil or Mexico.

The LatAm payments acceptance space has been growing fast, propelled primarily by domestic players (e.g., PagSeguro, Mercado Pago, Stone, etc.) offering mPOS terminals, digital payments, and other solutions. We expect further growth to be driven by fintechs such as dLocal and Ebanx, expanding outside the LatAm region.

Global PSPs such as Stripe, Adyen, and SumUp are increasing their presence in the region, focusing on the largest markets first. Due to its sheer size, Brazil is often the first entry point for international PSPs expanding to the region (e.g., Adyen opened an office in Brazil in 2011 and SumUp in 2013)

Instant Payment Schemes

Several LatAm countries have introduced instant payment initiatives running on account-to-account rails. The largest are state-owned such as PIX (Brazil) and CoDi (Mexico); although there are also privately-owned schemes in Colombia (Transfiya) and Peru (Yape and PLIN).

The Brazilian Central Bank launched PIX in 2020, which is rapidly growing in adoption. As of 2022, PIX reached ~$200 bil. in monthly transactions and has been used by ~130 mil. users. As one of the global poster children for A2A schemes, PIX presents serious challenges to legacy and cards-based payments infrastructure.

Other LatAm instant payment initiatives haven’t gained such massive traction as PIX. Since September 2019 to March 2022, ~$316 mil. transactions were processed via Mexican CoDi by ~17 mil. registered users. Private-led real-time payments initiatives in Colombia (Transfiya with < ~2 mil. users) and Peru (Yape and PLIN, each having < ~10 mil. users) are still in the early days of development. It is worth mentioning that Peru’s Central Bank mandated Yape and PLIN to interoperate from 2023 to eliminate the friction in instant payments; as a next stage the Peruvian regulator is planning to establish a general interoperability system to connect all fintechs and banks in the country.

Despite current relative success, instant payments schemes have the potential to disrupt the lucrative cards market, driving the growth of digital payments and opening new opportunities for LatAm fintechs.