The recent replacement of PayPal’s CEO after only two years in the role has sparked passionate discussion on what caused the decline of the original fintech unicorn. While, in retrospect, there have been some real missteps, we believe the more interesting question is what PayPal could yet become. Despite a decade of strategic drift, the company retains unique assets that no competitor can replicate quickly: an identity graph of 430 million people, two-sided distribution including 35 million merchants, financial and compliance infrastructure across 200 markets, and early leadership in agentic commerce.

Equity analysts are forecasting PayPal’s EBIT will shrink 23% over the next five years and public market investors seem to be pricing in a managed decline scenario at current share values. In the past few days, PayPal's depressed valuation has also reportedly attracted takeover interest. But 2026 doesn’t need to be the beginning of the end for what is arguably the original fintech unicorn. PayPal can commit to bold moves to evolve from being one of many digital wallet overlays to providing a programmable settlement and identity layer for the next era of commerce.

The Original Fintech Unicorn

PayPal is a fintech legend. Long before “fintech” was a sector, before Stripe, Square, or Apple Pay, PayPal was the easiest way to pay and be paid online.

PayPal’s initial growth was driven by solving two critical problems for consumers: hesitation to share sensitive payment card details with unknown, untrusted merchants in the early days of e-commerce and simplifying clunky checkout experiences in an era when few merchants had card vaults. People today forget how common it was for online checkout forms to require 100+ keystrokes across 20 fields; PayPal condensed the experience to an email, a password, and a few clicks. PayPal was also enormously valuable for sellers too: for a decade before Square launched in 2009 or Stripe in 2011, PayPal was the main way for small sellers to accept online payments, first on eBay, then across the open web. And its bold acquisition of Bill Me Later (now PayPal Credit, effectively the original buy-now-pay-later provider), purchased for $1 billion in the midst of a banking crisis, showed a shrewd instinct for identifying adjacent markets before they matured.

PayPal continued making bold bets in the early 2010s: it launched Mobile Express Checkout in 2010 when mobile devices accounted for just 2 percent of digital sales, acquired Braintree and Venmo for $800 million in 2013, and aggressively expanded internationally (international users grew from 28% of PayPal’s user base in 2005 to 60% by 2015). These moves enabled PayPal to grow its payment volume consistently at 20% annually for a decade.

It’s fair to say that the first era of digital commerce required PayPal. However, the characteristics that once made PayPal indispensable - security, checkout simplification, and democratized acceptance - are now table stakes in digital payments.

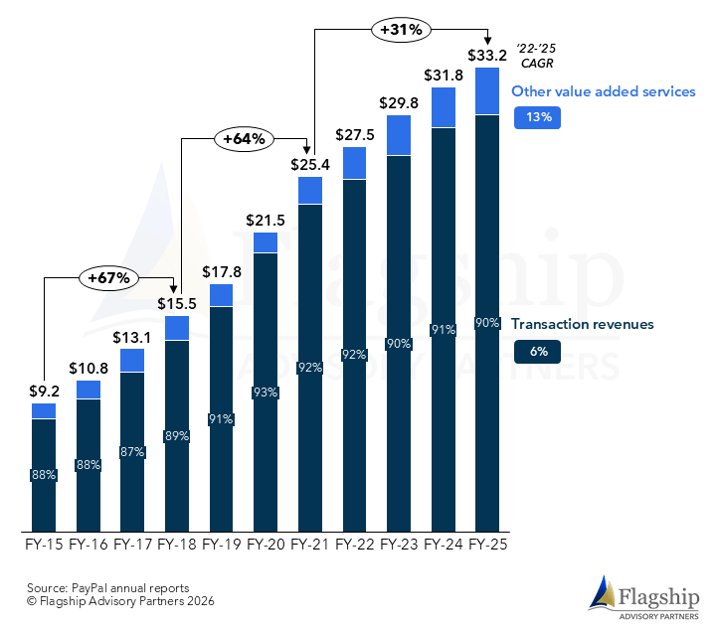

Figure 1: PayPal's Plateau

(gross revenue by type, billions of $)

A Decade of Strategic Drift

The structural shifts that undermined PayPal’s original value propositions have been visible for years, but the company’s actions have compounded, rather than compensated for the damage.

It’s no longer that hard to pay or be paid

There was real friction in digital payments until the last ten or so years but today nearly every bank app in North America and Europe (PayPal’s core markets) has built-in person-to-person payment capabilities, responsive checkout forms and autofill (either via merchant card vaults or browser-based autofill) are effectively universal, and it’s not hard to go from sign-up to accepting payments in minutes by using a PSP like Square or capabilities built into your business software. On top of all that, card tokenization platforms launched by Visa and Mastercard in 2014 opened the door to digital wallets like Apple Pay that leveraged biometrics and device-led identity to turbocharge data fulfilment and payment verification in one click. Merchants no longer rely on PayPal to drive conversion through payments ease. The effect can be seen in PayPal’s performance; it was able to ride the wave of that core value proposition into new markets and greater volumes with 60%+ annual account and revenue growth into 2021, that momentum has now tapered as the likes of Square, Shopify, Stripe and Apple Pay’s penetration has gathered pace.

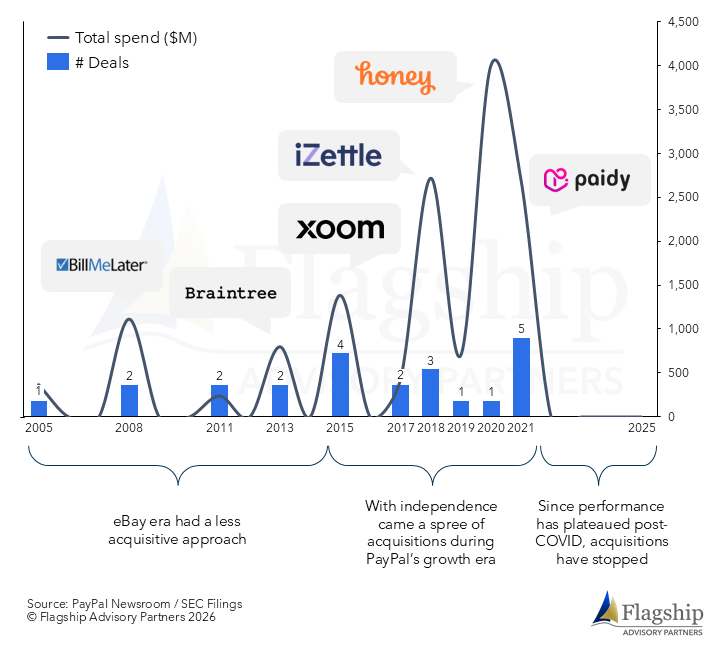

M&A without follow-through

Many of PayPal’s acquisitions over the last 10 years were in the right adjacent markets – markets that have proven to be unicorn-makers. The failure was not in the buying but in the building. Braintree, Venmo, Xoom, Paydiant, Hyperwallet, iZettle, Honey, and Bill Me Later have largely been operated as silos rather than integrated into a coherent product ecosystem or a single underlying platform (identity, risk, service, compliance, payments, customer data). On top of that, each company’s ability to innovate was hampered by PayPal’s corporate governance, leading to each business going from a leader within its market to losing ground relative to independent competitors. PayPal is a more complete company today with its acquisitions than it would have been without them, but arguably the company is also now less than the sum of its parts would have been if left to their own devices.

Figure 2: Missed M&A Opportunities

(PayPal M&A activity 2005-2025, total spend vs number of deals)

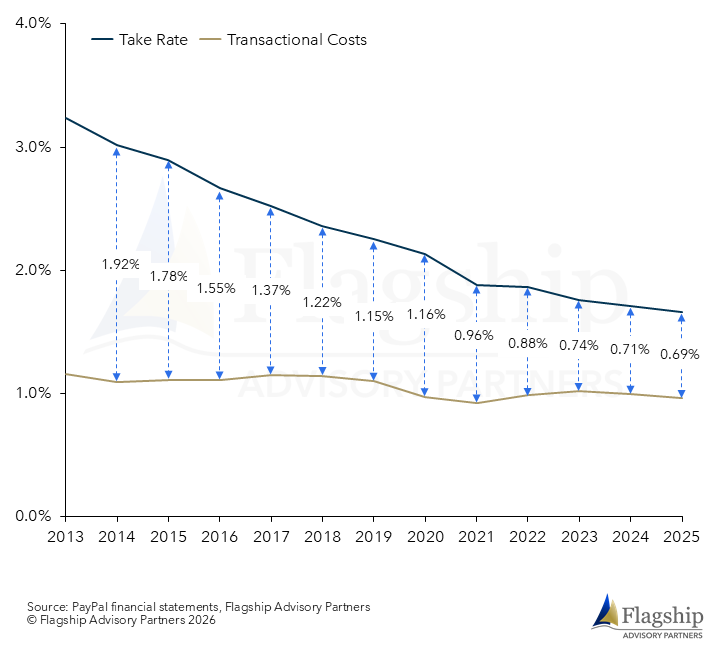

Surrendered economic levers

PayPal has grown dramatically (540%) since it was spun off from eBay in 2015, but it has also price-competed its way to that growth. The company’s take rate (excluding credit and value-added services) has gone from 2.9% in 2015 to 1.66% in 2025. This is partly due to adding new, lower-margin businesses around branded checkout but it’s not entirely a mix issue: equity analysts we follow estimate that PayPal’s take rate has declined for the past ten years across every business except P2P: branded checkout, merchant services, unbranded processing, eBay, Braintree, Venmo – every single business is earning less as a percent of volume in 2025 than it was ten years ago[1].

Exacerbating this trend somewhat is PayPal’s 2016 agreement to stop steering customers away from card-funded transactions as part of a deal with Visa and Mastercard. While this deal came with meaningful benefits (access to V/MC tokenization, defusing the threat of additional network fees and unlocking incentives, bank marketing) it also seriously handicapped the company’s most powerful economic lever – its ability to steer customers towards using lower-cost bank rails – and likely created complacency around leaning into stablecoins as a new settlement system.

Figure 3: PayPal Transactional Economics Analysis

(transaction revenues less transaction expense and transaction losses, as a % of TPV)

A revolving door at the top

PayPal has cycled through three CEOs in three years, alternating between “product” and “business” archetypes, and each transition has consumed 12-18 months of organizational energy. The pattern suggests less a talent problem than a governance one; repeated CEO transitions have reset priorities before strategic bets could compound. To transform the company, PayPal’s board must stand behind Lores, even if results take some time. He needs to bring back on leaders with payments knowledge and product vision, and those leaders need to empower their teams to think and act long-term.

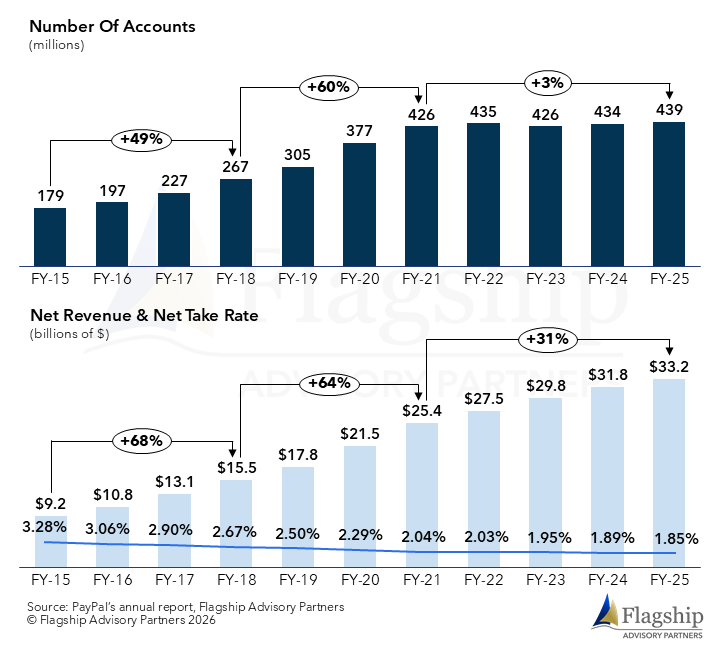

Figure 4: Signs Of Strategic Drift

(PayPal number of accounts, net revenue & take rate)

The Assets Most Critics Overlook

The bearish commentary has focused almost entirely on what PayPal has lost, which is fair as far as it goes, but it understates the structural assets that the company still has and that no competitor can replicate quickly. These assets are underleveraged today but could be decisive in the next era of commerce.

-

Identity graph

PayPal has more than 430 million accounts with verified identity, cross-border transaction history and years of fraud and trust data. In a world moving toward agentic AI, where bot traffic has increased from one-third of web visits in 2019 to one-half in 2024, being able to sort out real users (and their delegated agents) from fraudsters will be a valuable resource.

-

Two-sided distribution

PayPal operates multiple consumer brands (PayPal, Venmo, Xoom, Paidy) and merchant processing platforms (Braintree, Zettle, PPCP). That two-sided network – branded and unbranded, consumer and merchant, pay now and pay later – creates a flywheel that is difficult to replicate even if individual components are under pressure. Recent data confirms it still works: full-stack PayPal deployments combining modern checkout, biometric enablement, BNPL messaging and co-marketing drove double-digit branded TPV growth at several merchants during Cyber 5 2025, according to UBS.

-

Settlement control

PayPal’s infrastructure includes direct bank rails (lower cost than cards), its PYUSD stablecoin (with programmability potential for micropayments and cross-border settlement), direct merchant contracts, and the ability to net FX flows across global entities. If merchants who receive PayPal payouts also use PayPal to make subsequent B2B purchases, that creates a closed-loop funding source with near-zero marginal cost. PayPal could leverage these capabilities not only for novel functionality but also to reverse the long-term status of its funding costs and resulting compression of its net spread.

-

A head start in agentic commerce

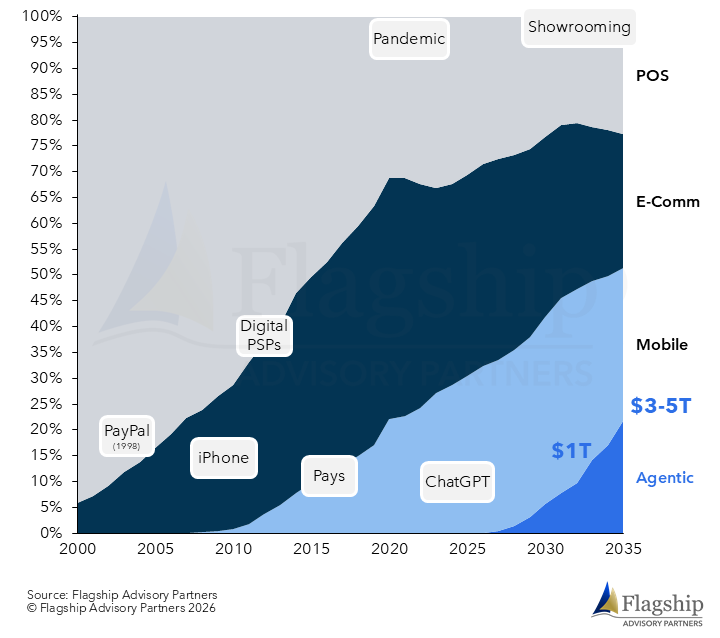

This is perhaps the most underappreciated asset. PayPal has established collaborations with OpenAI, Google Cloud, Microsoft, and Perplexity to integrate its checkout into AI-powered shopping surfaces. It has built an agent-ready transaction framework (“agent ready”) and “store sync” infrastructure that provides AI agents with the structured commerce data they need to operate effectively. Flagship estimates that by 2035, $3–5 trillion of US consumer payments will flow through AI agents. The infrastructure for those transactions is being built now, and PayPal is at the table.

Reinventing PayPal For The Next 10 Years

Over the last two years, under its last CEO, PayPal was making a lot of the right investments to transform and update its existing business: Fastlane, biometric authentication, platform integration, more pricing discipline on Braintree, and progress on monetizing Venmo. Those actions should continue and will result in a stronger PayPal, but not a fundamentally different or future-proof company.

We believe PayPal can return to market leadership through bold investments across four fronts:

1. From wallet to network

PayPal has some structural disadvantages relative to its competitors: Apple controls the device layer, banks control primary accounts, and Stripe is embedded across SaaS. Given those challenges, PayPal may not be able to be everyone's preferred wallet. If PayPal can't win every wallet, it should be the network that connects them.

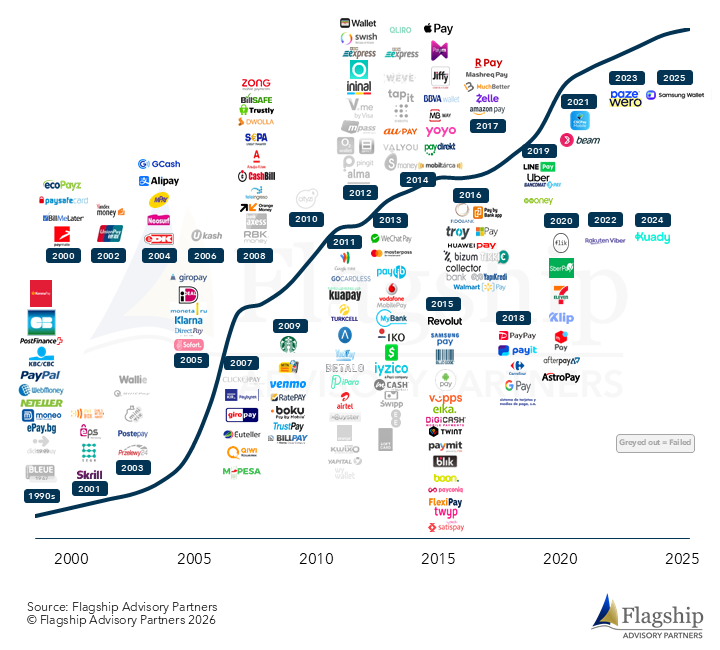

PayPal already enables consumers to use Apple Pay and Google Pay in its branded checkout and it enables merchants to accept Alipay and eight other APMs through its API. It should accelerate the PayPal World program it kicked off last year: provide interoperable rails for any wallet in the world to work wherever PayPal is accepted and vice versa. Alipay, Paytm, CashU, MercadoPago, GCash, Paze, Zelle, Wero, and others should all be able to transact at PayPal merchants seamlessly. Merchants should be able to think of PayPal not as one of many wallets on their checkout page, but instead as the portal to whatever payment method their global customers use.

Figure 5: Digital Wallet Fragmentation

(global digital wallet launches)

Underneath this expansion, PayPal needs to get into the business of actual money movement, not just being a front end. Cards have grown from funding 60% of PayPal and Venmo (ex-Braintree) in 2014 to nearly 70% today. To reverse that trend, PayPal should use PYUSD to create instant, cheap, programmable money settlement infrastructure between its users, merchants, partners, and other payment methods.

2. Win daily commerce

PayPal is broadly accepted online (84% of the top 100 US retailers offer it at checkout) but it barely exists in-store, where most spending still happens. Offline is still 80% of retail but only 2% of PayPal's volume. Previous attempts to close that gap, including phone-number-and-PIN at Home Depot in 2012 or QR codes during the pandemic, failed because they asked consumers to adopt a worse in-store experience than the card they already had in their pocket.

PayPal might need to build its own settlement system online, but in the physical world it should just ride the card rails. They have had access to card network tokenization (VTS and MDES) since 2016 but haven’t done much with it. PayPal offers a debit card and it’s growing quickly, but every PayPal customer should be able to use PayPal (and PayPal Credit) in-store by tapping their phone wherever Visa or Mastercard are accepted. If the card networks’ staged wallet rules are a blocker, PayPal should think more creatively, such as putting a line of credit or PYUSD in between every card purchase and every funding event.

There is clear evidence that in-store can be a huge growth vector for PayPal: Klarna and Affirm have signed up 5+ million people in the U.S. for cards and in-store is now more than 15% of their total spend, with 25% of card usage in categories those companies didn’t historically serve online.

Venmo can be PayPal’s secret weapon in this battle. A debit card without a daily app relationship behind it is just another piece of plastic, but Venmo is the app 100 million younger people already use regularly. The product needs to lean into the things that keep younger consumers engaged daily — real-time spending control across every merchant relationship, flexible payments that let users change funding source or pay over time before, during, or after a transaction, and a social layer that reinforces the habit.

3. Own agentic commerce

When an AI agent books a flight, reorders supplies, or comparison-shops across dozens of merchants in seconds, it needs three things: a verified identity to transact on someone's behalf, a set of rules governing what it can spend and where, and structured commerce data to act on. PayPal's identity graph solves the first and its digital wallet is a natural control center for the second. PayPal has already started building the infrastructure (store sync) for the third and its broad partnerships with AI companies give PayPal a shot at being the default payment layer inside AI-powered shopping surfaces.

The competitive dynamics here are different from traditional e-commerce because agents don't see buttons, don't have brand loyalty, and don't care about checkout UX. Agents care about clear instructions, structured data, API reliability, efficient settlement, and strong post-purchase protections. That is a combination of needs that PayPal is uniquely positioned to support. Longer-term, PYUSD also gives PayPal a programmable settlement capability that can handle the micropayments, conditional logic, and machine-speed escrow that may become more common with agentic transactions.

Figure 6: Agentic AI Adoption

(US digital consumer payments channel mix, est.)

4. Become easier to work with and work at

None of the above matters if the company cannot execute faster than it has in the last decade. PayPal operates at least seven distinct product surfaces each with its own onboarding, identity layer, and merchant integration. As we mentioned earlier, internally that fragmentation translates into duplicated systems, competing roadmaps, and a bureaucratic overhead that slows everything down. Externally, it means merchants and distribution partners face unnecessary friction. One telling example: unlike most alternative payment methods, PayPal requires every end-merchant to sign a direct contract rather than allowing distribution partners to act as aggregators. That single policy choice locks PayPal out of the long tail of merchants that other APMs can reach through aggregators like Stripe, Adyen, Nuvei, PPRO and others.

Alex Chriss kicked off a technology transformation program to integrate PayPal into one platform, with one customer profile, and one product development process internally. Realizing that vision will be an expensive, multi-year effort but it must be done. This is unglamorous work but it is the difference between a company that articulates a compelling strategy and one that actually delivers it.

This may only be possible as a private company

It is worth asking whether the reinvention described above is achievable under public market scrutiny. PayPal trades at ~7.5x forward earnings with a market capitalization of roughly $39 billion, generating ~$6 billion in annual free cash flow. The market is pricing the company for slow, managed decline and quarterly earnings pressure reinforces the incentive to optimize for near-term transaction margin dollars rather than invest in platform transformation.

Reinventing rails is a 3–5 year capital cycle. Public markets rarely tolerate visible earnings drag over that timeline. A take-private transaction would provide the capital, the refreshed governance, and most importantly the time horizon necessary to execute a genuine platform reinvention without quarterly margin scrutiny. However, any financial sponsor (or strategic buyer) would have to be prepared for substantial investment and a highly complex transformation program.

The last 10 years don’t have to define the next 30

PayPal’s decline serves as a reminder to every fintech company that incumbency is not king. In an increasingly commoditized and crowded payments industry, it is essential to constantly refine and refresh customer relevance, even if that means making bold pivots into new markets.

The PayPal story is not over. The company that solved online trust in 1998, acquired the first BNPL provider in 2008, and built a 430-million-account global network still has the raw materials to be relevant in 2035. The question is whether PayPal’s new leadership is willing to use them and what is the best ownership structure to enable bold reinvention.

Please do not hesitate to contact Ben Brown at Ben@FlagshipAP.com and Will Hay at Will@FlagshipAP.com with comments or questions.

[1] Unbranded processing excludes Braintree. Braintree excludes PayPal button and Gateway. Venmo excludes P2P and instant transfer revenue.