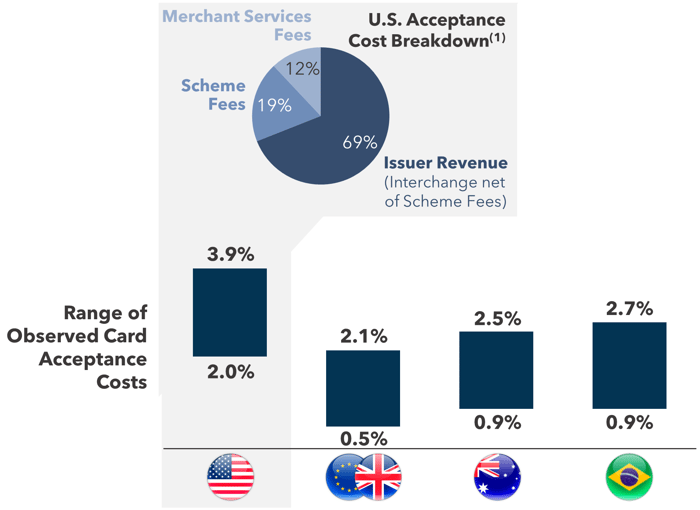

Technology breeds efficiency, at least under normal circumstances. U.S. card acceptance falls into the unusual circumstances category. Despite having the world’s second largest digital economy (behind China), the U.S. has the highest costs of payments (as shown in Figure 1) among developed global markets driven primarily by the high cost of cards. There is a long history behind the high cost of cards in the U.S., and a lot of atrophy towards change. However, we do not see this lasting forever. We believe that market forces will eventually disrupt the cards ecosystem that drives the high costs of payments. In fact, we can already see some of this disruption writing on the wall.

FIGURE 1: Average Credit & Debit Card Acceptance Costs in Select Regions

1Estimated market average for U.S. V/MC cost allocation

Source: Flagship Advisory Partners estimates

How Did the U.S. Get to Such Persistent High Cost of Payments?

U.S. interchange and scheme fees have increased for many years. Visa and MasterCard compete for issuing business in part, based on price. Introducing new, more expensive interchange categories, and increasing merchant acquiring scheme fees in order to fund incentives for issuers has been a winning strategy for many years. The price-taking merchant acceptance side of the ecosystem has no real means of defense; deciding not to accept Visa or Mastercard is not practical. Regulators appear to have little appetite to re-engage on further regulation of interchange following the Durbin amendment that regulated certain categories of debit card interchange more than a decade ago. Such government price setting is generally frowned upon in the U.S. and some saw the Durbin amendment as questionable public policy (i.e., simply a transfer of wealth from one powerful set of companies to another with little benefit to consumers or small businesses).

Seeking Out Alternative Payment Methods

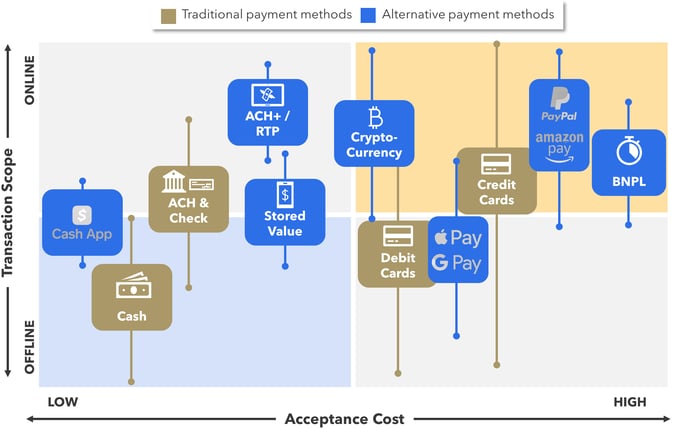

U.S. merchants are constantly on the lookout for tactics to reduce the high costs of card acceptance. Finding and supporting lower cost alternative payment methods is the easiest way offset the cost of cards. Figure 2 illustrates the landscape for U.S. payment methods illustrating relative cost and range of usability.

FIGURE 2: U.S. Payment Method Landscape

Source: Flagship Advisory Partners market observations

The challenge today is that there simply is no silver bullet alternative payment method (‘APM’) that provides low costs, robust acceptance enablement, strong UX, and controlled risk. Many U.S. APMs are used today for a narrow set of use cases (depicted as the range on Figure 2) or have other flaws.

• ACH and e-checks can be lower cost but lack broad acceptance coverage.

• Real-time banking rails have yet to translate into mass acceptance of bank payments (Zelle, which rides the RTP rails, can be used for C2B, but is driving little to no C2B volumes today).

• PayPal has not yet pushed to compete on price with cards, for example by enabling Venmo linked to bank payments for merchant acceptance. In fact, PayPal maintains a symbiosis of sorts with the card schemes, including strategic partnerships with Visa and MasterCard.

• Cryptocurrency payment acceptance is still nascent with a fairly broad range of costs (1%-2.5%), but we expect major acceleration in crypto payments (we illustrate the growth of C2B crypto commerce here).

• BNPL is one of the most expensive payment methods for merchants to accept, but it demonstrates its utility by reducing consumer purchasing burden for high-value transactions.

• Lastly, other mobile wallets and payment methods also rely primarily on card funding, which makes them as costly or more costly than cards to accept.

While no one of these APMs is a threat to the cards ecosystem today, each is nibbling at the edges with a potential for longer-term disruption. At the heart of disruption potential is the evolution of real-time banking infrastructure. Real-time bank payment rails are an ideal foundation for development of APMs as seen throughout the rest of the world. Any number of scaled mobile apps/wallets (PayPal, CashApp, Dunkin, etc.) could use such rails to displace the costs of cards.

The viability of real-time payments in the U.S. is still challenging, however. The core infrastructure is now largely in place. RTP, operated by The Clearing House that also enables much of the U.S. ACH system arrived in market five years ago and in 2021 processed more than 1.8 billion transactions. FedNow, operated by the Federal Reserve, is a newer infrastructure set for go-live in 2023.

U.S. banking remains highly fragmented however (there are more than 4,000 FDIC insured banks), which limits the pace of any form of banking rails rollout. In a recent study by Volante Technologies, only 15% of 160 surveyed banks and credit unions were connected to The Clearing House’s RTP network, citing that a new payment type was a complex proposition to implement and/or caused fraud/security concerns since RTP transactions are irrevocable after settlement. Note however that a majority (70%+) of deposit accounts (via the largest banks) reside with banks that are technically positioned to support RTP. RTP is also only a bank clearing network and not a full payment scheme. Others will need to deliver the full proposition that is an RTP-based payment scheme (brand, acceptance infrastructure, rules, risk management, etc.).

The banks themselves are generally reluctant to challenge the cards ecosystem with their own RTP-based scheme (we all know the golden goose fable after all). However, there is at least a debate ongoing as noted in this WSJ article. According to the Wall Street Journal, Wells Fargo and Bank of America are in favor of pushing Zelle towards C2B payments while JP Morgan is concerned about moving too fast given the need for supporting fraud management infrastructure, with other major banks undecided. Zelle is already used on a limited basis for consumer payments to small businesses, with these volumes growing 162% in 2021 (according to the WSJ). Considering that banks are no longer shareholders of V/MC, there is a prize to pursue (V/MC’s scheme fees in the U.S. are extra juicy). However, we are skeptics of any coalition relying on many banks as a force of disruption. For decades in fintech, we observe a clear pattern whereby the more parties involved in a coalition action, the less impactful and disruptive the coalition.

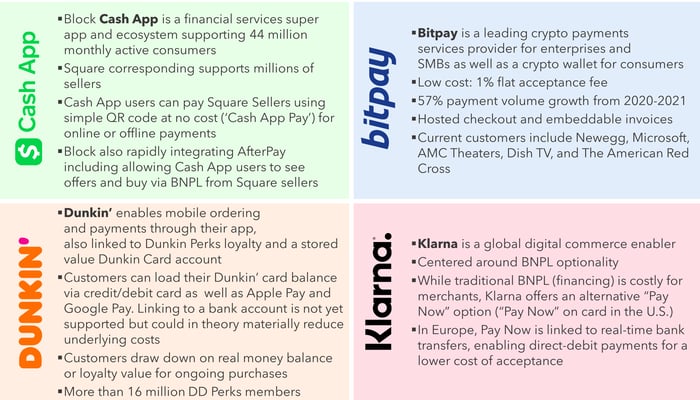

FIGURE 3: Select U.S. Alternative Payment Method Examples

Source: Company websites, Flagship Advisory Partners market observations

Source: Company websites, Flagship Advisory Partners market observations

In Figure 3, we summarize a handful of the models that we see as potentially most disruptive in the long-run in the U.S. Block is positioned to drive long-term disruption of the cost of cards. Both Cash App and Square have a significant market share of consumers and SMB’s respectively. Combining this on-us potential (including growth in the coming years) with the ability to also leverage BNPL, crypto payments, and payments backed by RTP fundings and the disruption potential becomes compelling. The potential could accelerate with partnerships within the enterprise merchant segment to leverage Block’s ecosystem.

Merchant in-app wallets (leveraging stored value) such as Dunkin’ can also reduce card acceptance costs by expanding the magnitude of stored value retained within their ecosystems and by shifting from linked cards to linked bank accounts. Merchants such as Dunkin’ are unlikely to solve the gaps of RTP (i.e., rules and risk mgmt.) on their own, but working with partners such as Plaid, the scenario become more interesting.

Klarna and BNPL are premium priced payment methods given the risk they take, and the sales conversion delivered. But in Europe, Klarna also delivers Pay-Now via real-time bank transfer. Noting the gaps in RTP infrastructure mentioned previously, we would expect Klarna to ultimately introduce a bank-powered Pay-Now option at some point.

Crypto payments are years away from mainstream scale, but the disruption potential becomes interesting if key actors are able to deliver low-cost payments such as those marketed by Bitpay (1.0% acceptance).

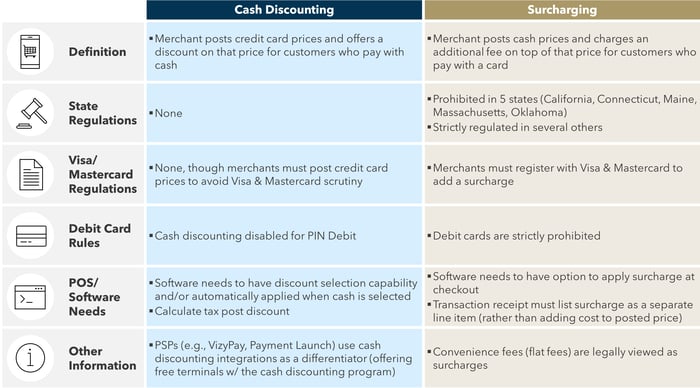

Cash Discounting: An Oddly Common Tactic in the U.S.

As merchants await more viable, cost-efficient alternative payment methods, many merchants today actively steer POS customers towards cash using cash discounting (an interesting oddity in what is otherwise a modern digital economy). Cash discounting is heavily marketed by PSPs and merchant acquirers in the U.S. Often used synonymously (and incorrectly, as we clarify in Figure 3) with surcharging, merchants using cash discounting by posting the price of goods and services as the “card rate” while offering a lower price from the posted (card) price to customers that are paying with cash. For some U.S. ISOs, half of new POS merchants implement cash discounting. These companies push cash discounting programs as a means of “protecting” merchants from excess card fees, while driving value-added services revenues for themselves.

FIGURE 4: Cash Discounting vs. Surcharging

Source: Payment Cloud, CardFellow, VizyPay, Flagship market research and observations

Source: Payment Cloud, CardFellow, VizyPay, Flagship market research and observations

Looking Forward: Fintech Disruption of Consumer Payments

The U.S. cards ecosystem is amazingly effective as a driver of U.S. commerce and a huge revenue pool benefiting thousands of financial services providers. Visa, Mastercard, Amex, Discover, and their broad network of partners, did an amazing job of solving payments in the highly fragmented U.S. banking market. The staying power of this ecosystem cannot be underestimated, as many potential disruptions have come and gone (decoupled debit, merchant coalitions, etc.). But the fact remains that the U.S. cards ecosystem is unusually expensive considering the scale and digitization of the economy (the majority of U.S. card payments volume is remote commerce, not physical commerce).

We believe that disruption of this high cost of payments will come. The size of the prize is simply too big to go untouched, especially considering the availability of disruptive technologies. We expect the legacy control of the market by incumbents, which drives the current commercial stasis on cards, to be threatened by new models driven by mobile commerce, real-time banking, and crypto currencies. Just don’t quote us on when.

Please do not hesitate to contact Rom Mascetti at Rom@FlagshipAP.com or Joel Van Arsdale Joel@FlagshipAP.com with comments or questions.