Ant Group, the parent company of Chinese digital payments and fintech giant Alipay, recently filed an IPO prospectus which demonstrates the value-creation potential of fintech: for shareholders, consumers, and partners. Ant’s 674-page prospectus makes for fascinating reading, and strikingly illustrates three key takeaways:

- Ant Group is a payments and fintech behemoth with massive scale and breadth of revenue;

- Ant has successfully expanded Alipay from a payment method into a financial services supermarket, and is now expanding into what it terms “daily life services”; and,

- Ant’s development and business model is the result of unique circumstances, which while not be replicable in the North America and European markets given their respective state of maturity, still offers valuable lessons for fintech leaders in developing markets.

Scale and Breadth

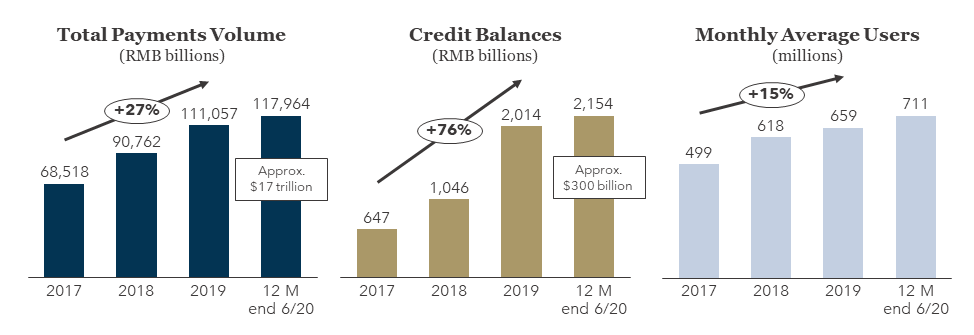

Ant Group and its Alipay payment method are uniquely huge, with 711 million average users, $17 trillion in annual payments volume, $300 billion in consumer and SME credit balances, and $600 billion in investment assets under management. In terms of market shares in China, this represents 47% of the population, 55% of digital payments, 10% of consumer and SME credit balances, and 2% of personal investable assets, respectively.

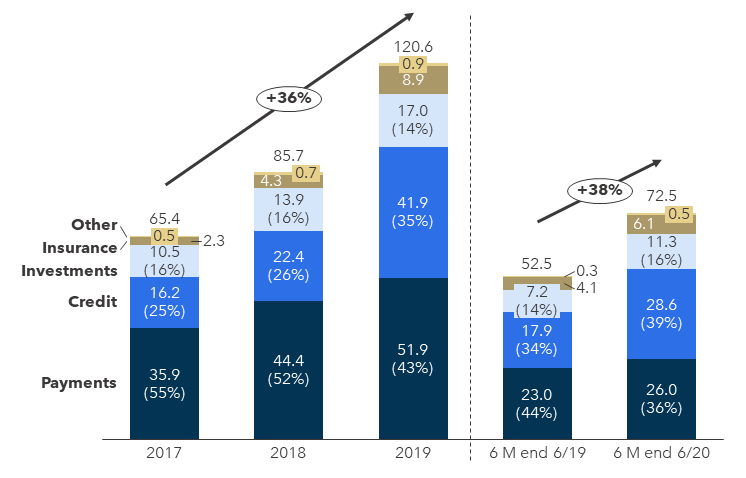

FIGURE 1: Ant Group Revenue Growth and Mix

(RMB trillions)

Services Expansion

Ant Group has grown revenue and profitability with a 30%+ CAGR between 2017 and 2019, driven heavily by its successful expansion into distributing credit, investments and insurance. In 2019, these other non-payments expansions comprised 57% of gross revenues. Credit, where Ant acts as a distributor, score provider, and servicer for others lending (98% of lending is off balance sheet), has been the primary growth driver beyond payments. In the six months ending June 2020, gross credit revenue surpassed gross payments revenue. Payments is still very lucrative however, with net revenue equivalent to 4.7% of volume during 2019.

Ant, via the Alipay platform, is now expanding beyond financial services and into “daily life services”, which include over 1,000 mobility and local services and over 2 million “mini apps” within the main Alipay app. During the past 12 months, these services were utilized by an impressive 60% of Ant’s total users.

Alibaba remains important to Ant’s payments business (and overall ecosystem) contributing RMB 9.2 trillion in payments revenue to Ant in 2019, or 18% of total gross payments revenue (diluted by the significantly lower gross margins on payments volume of 0.60%). Ant investors will be comforted to know that most contracts with Alibaba are 50-year contracts with a subsequent 50-year auto renewal.

FIGURE 2: Ant Group Key Metrics

Key Lessons

Ant Group’s trajectory is the result of highly unique scale, which is not replicable outside of China, but the diversity of revenue bodes well for fintechs in other growth markets. Alipay clearly demonstrates the potential of multi-service platform emanating from payments. We caution the applicability of this lesson to North America and Europe, however, where consumer behaviors are not consistent with Alipay’s “one app to rule them all” approach. Still, there are important lessons that fintech providers globally can draw from Ant’s success.

- Partnerships are core to fintech: Ant emphasizes that its business model is to partner with banks and other financial services providers and generate revenues from distribution to its user base, rather than compete head-on as the owner of the underlying product.

- The future of payments is integrated services: As illustrated by Ant’s revenue expansion and ecosystem approach, integrating payments into other services (and vice versa) is a powerful generator of usage and revenues (including B2C and B2B integrated services). This trend is playing out globally in integrated payments and business services as we describe in a recent article [click here for article], though integrated consumer use cases generally lag Ant’s success.

- Transactional credit is a large revenue opportunity: Alipay demonstrates the potential of providing easy-to-use, digitally delivered credit to finance purchases (which is a market still growing into its potential in most global markets). Many fintechs have focused on the opportunity, most notably Klarna, but traditional providers of unsecured credit must innovate in order to compete with fintechs in this segment of the market.New Paragraph

To share your views or discuss those above, please contact Erik Howell at Erik@FlagshipAP.com.