The most lucrative, fastest growing merchant payments companies are not acquirers. Payment facilitators such as Stripe, PayPal, Sumup, d-local, Ebanx, Mercado Pago, PagSeguro, Stone, Shopify, Intuit, Mollie, and others reinvented the market, extracting huge profits by leveraging digital technology to address the long-tail of small merchant payments. Acquirers largely missed the boat and have often relegated themselves to basis point scraps of acquiring for these high growth payfacs.

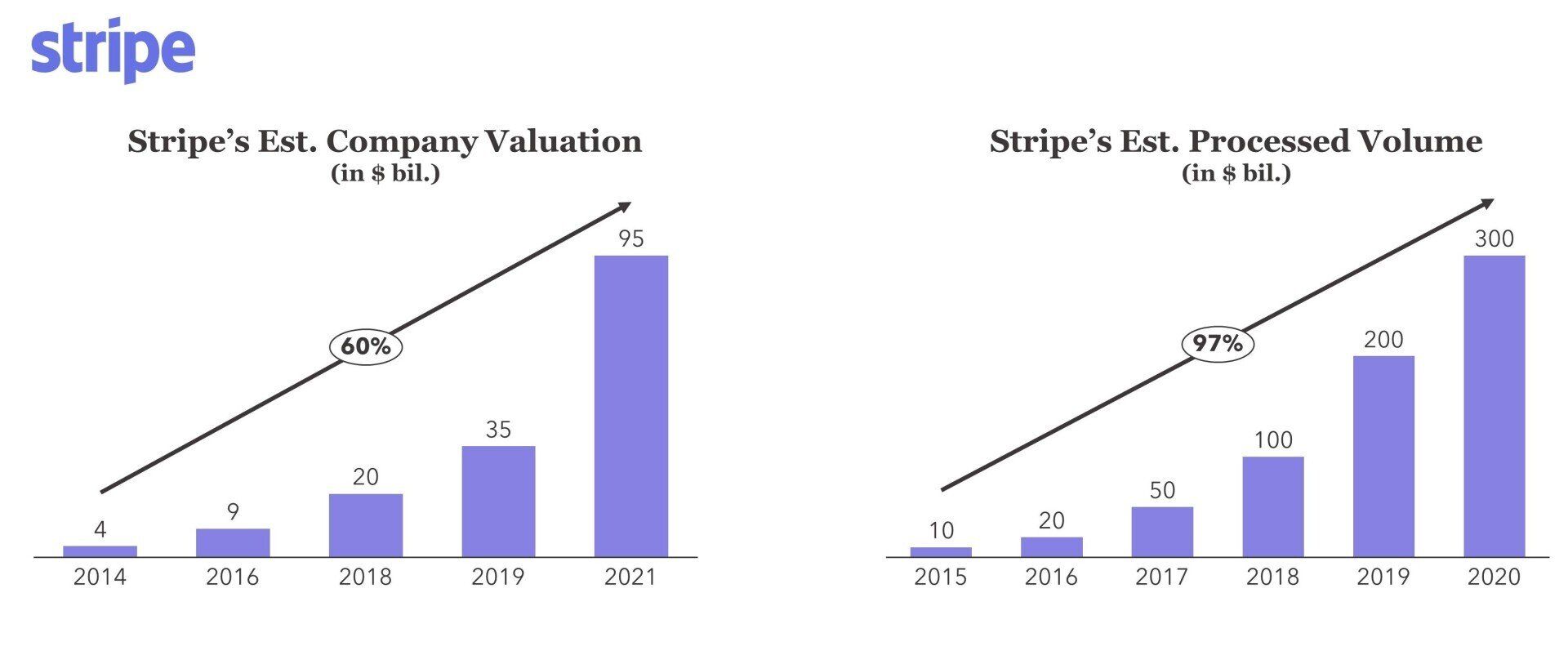

Payment facilitation began with PayPal years ago. PayPal now works with many millions of merchants around the world. Stripe also supports more than 1 million merchants globally as does Sumup. Most of these merchants are considered unprofitable by acquirers. (Psst, hey acquirers, Stripe made $1.6 billion of net revenue with a net take rate of 53 bps in 2020). Payment facilitators now have a market cap that exceeds that of all acquirers globally (including Stripe’s c. $100B valuation and PayPal’s c. $300B valuation).

FIGURE 1: Estimated Stripe Processed Volume and Market Capitalization

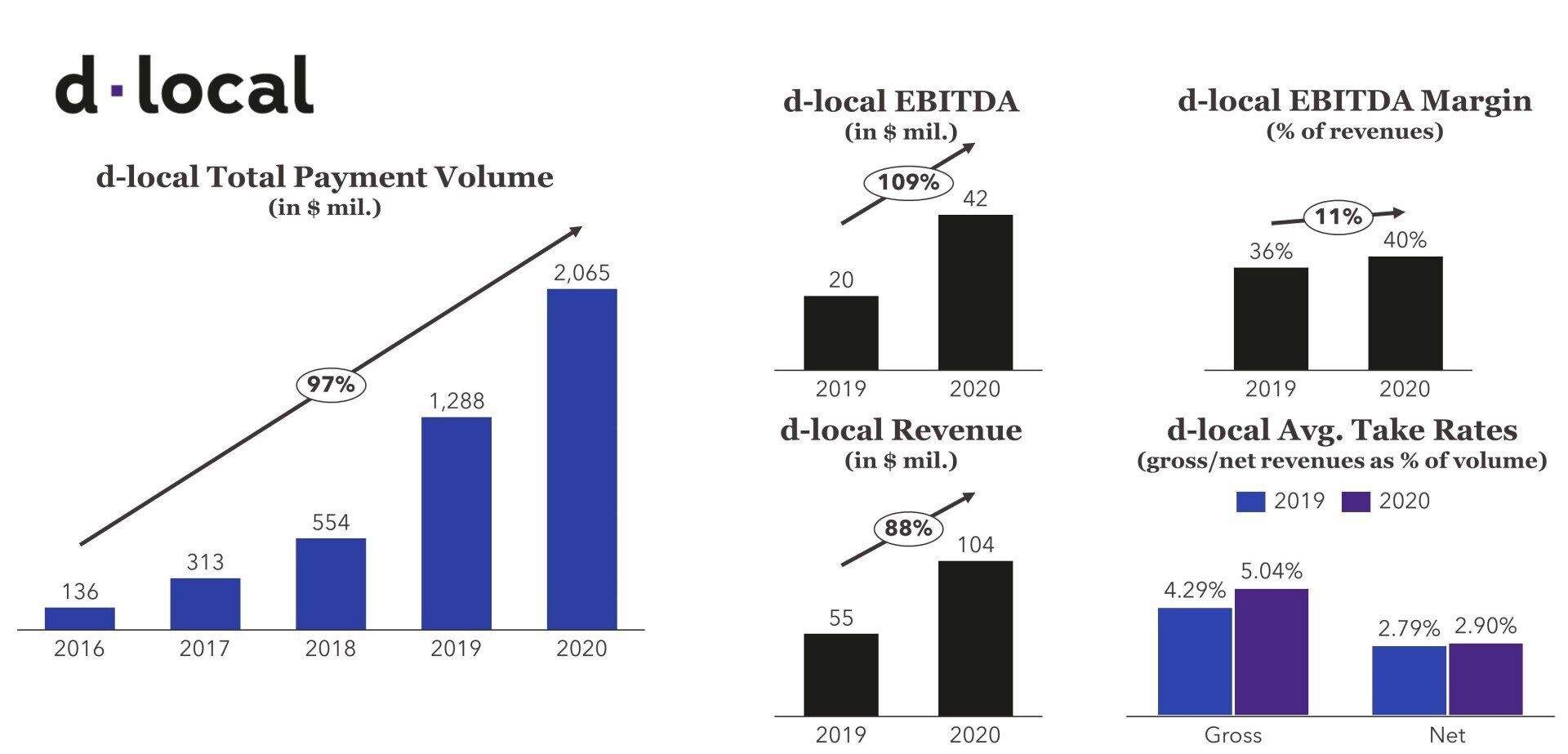

While many of these payfacs focus on small merchants, there are also payfacs thriving with larger merchants with a focus on the longtail of geographic markets. d-local, who recently filed for IPO, is reinventing the market for payment services in far-flung developing markets, making it easy for merchants to achieve local payment advantages without having to incur the pain of legally localizing. In exchange for this valuable payment facilitation service, d-local earns a juicy 2.9% net and 5.0% gross take rate (see Figure 2). Visa and MasterCard are certainly happy to have relaxed their rules and opened the world to payment facilitators, who now account for much (if not most) of the growth in global merchant acceptance, particularly in developing markets.

FIGURE 2: d-local Financial Highlights

Acquirers largely failed to innovate and adapt to the promise offered by mobile and cloud technologies, and to pursue the high-growth revenue pools of the longtail of merchants and countries. Payfacs thrive with digital marketing, easy sign-up, real-time responses, and fully digital servicing environments. Payfacs also rapidly globalize with products and tech stacks designed to connect into new acquirers and to support new languages, currencies, and payments methods. Acquirers, on the other hand, tend to be stuck in their domestic markets while continuously working to modernize their technology and customer experience. M&A has driven much of the growth of the world’s largest acquirers, but this M&A comes at the price of having to execute on challenging, post-merger integration work. Payfacs tend to focus on organic development and maintaining clean, agile tech stacks. Acquirers also failed to embrace SaaS platforms and developers, the distribution secret to the success of many payment facilitators. A developer/platform-first approach allows payfacs to deeply integrate into commerce bundles and to achieve highly scalable and profitable customer acquisition models.

Acquirers must continue to strive for reinvention, following the lead set by payment facilitators. The massive, longtail of small merchants can be highly profitable with the right digital operating and distribution models.

Please do not hesitate to contact Joel Van Arsdale Joel@FlagshipAP.com, with comments or questions.