Flagship published insights across a diverse set of topics in 2022, including integrated payments, crypto, open banking, payfacs, M&A, neobanks, SoftPOS, Banking-as-a-Service (BaaS), the impact of inflation, B2B payments, spend management, and many others. Below we review and summarize our most popular articles of the past year.

The rise of Banking-as-a-Service (BaaS), in parallel with our commentary on the muted adoption of open banking payments generated significant reaction and healthy debate. Other topics which captured our audience’s attention entailed our reporting on Stripe’s remarkable 2021 performance, the historical evolution of SoftPOS and its potential for growth in 2023, and our proprietary analysis on the shifting market dynamics in U.S. merchant payments.

Links to our top-read articles here:

1. Banking-as-a-Service (BaaS) Fintechs Coming to Age to Fuel Integrated Finance Needs

2. European A2A Schemes Thriving, Not Yet Open Banking Payments

3. SoftPOS is Ready for Prime Time in 2023

4. Infographic: Stripe Setting the Performance Bar in Fintech

5. M&A No Longer the Key Driver of Consolidation in U.S. Merchant Payments

1. Banking-as-a-Service (BaaS) Fintechs Coming to Age to Fuel Integrated Finance Needs

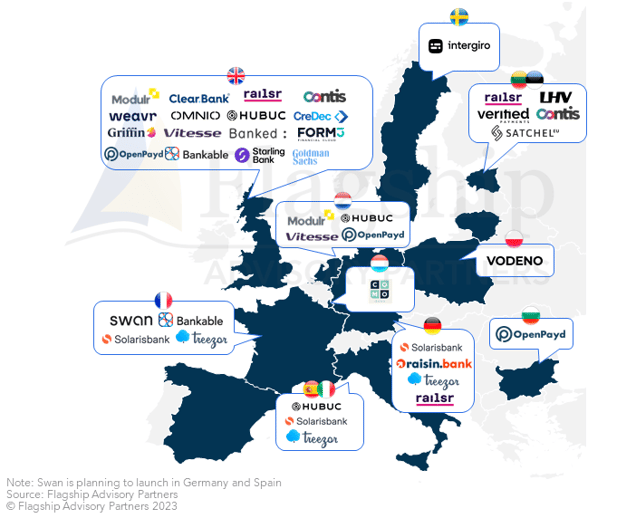

As the focus of our most-read article in 2022, Banking-as-a-Service (BaaS) enables any company to embed integrated financial services. The category came of age in 2022 with an influx of funding, the rapid proliferation of fintechs (including scaled players), and maturity in product setting the scene for widespread disruption of financial services distribution in 2023 and beyond.

FIGURE 1: European Landscape of BaaS Providers (2022; select players, based on office locations and license approvals)

2. European A2A Schemes Thriving, Not Yet Open Banking Payments

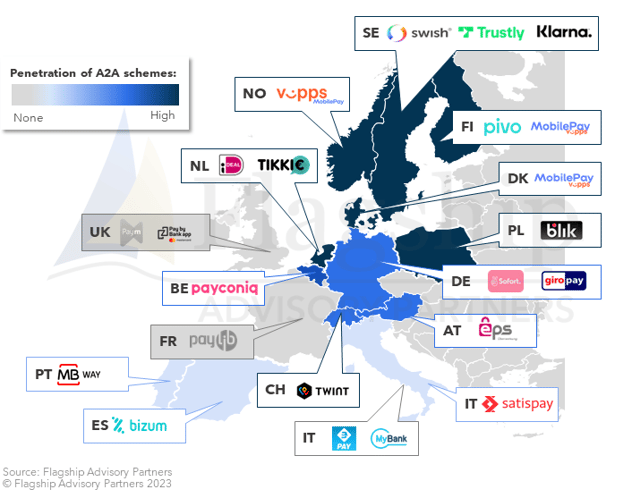

In parallel, our views on the unmet expectations European open banking payments generated healthy online debate. Open banking payment adoption remains muted and faces adoption challenges given the traction of A2A APM schemes in certain markets, and we went as far as calling open banking payments a solution in search of a problem. We do however remain optimistic that structural impediments will be removed, driving an ongoing expansion of PIS volumes, and that additional verticals and use cases will gain traction increasing its overall relevance.

FIGURE 2: Landscape of Select European A2A APM Schemes (2022; select players)

3. SoftPOS is Ready for Prime Time in 2023

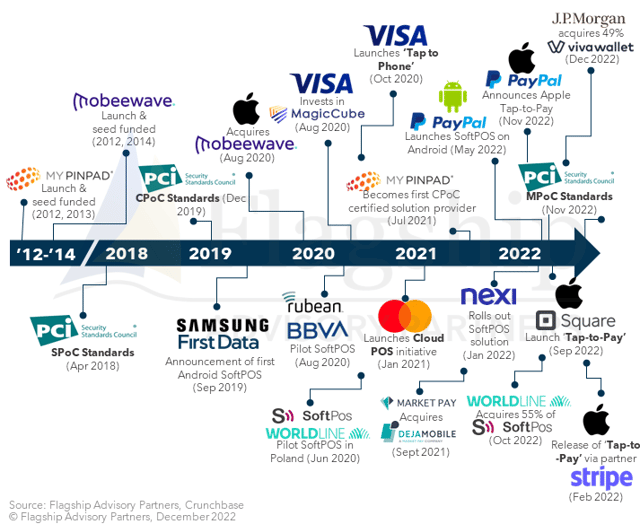

SoftPOS progressed slowly over the last decade, but is finally ready for the mass market with the launch of the most recent set of standards (MPoC). Our year-end article highlighted the importance of these new standards, which will address many historical constraints associated with SoftPOS giving rise to rapid scaling in the years to come. We believe that 2023 is the year SoftPOS takes off in earnest.

FIGURE 3: Select Events & Key Milestones in SoftPOS Evolution (2022)

4. Stripe Setting the Performance Bar in Fintech

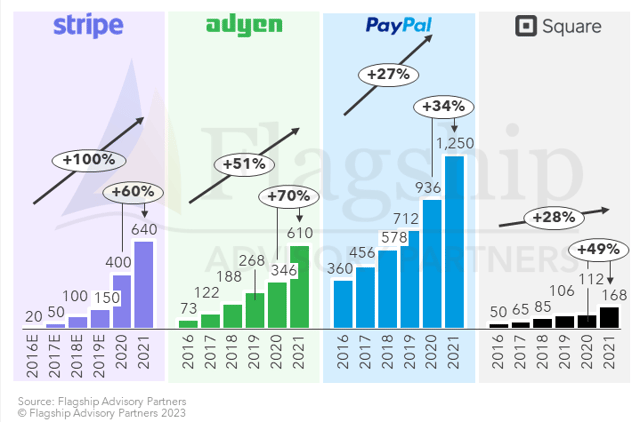

Stripe remains a darling of the fintech ecosystem, and our infographic highlighted its remarkable performance in 2021. Stripe outperformed peers in volume growth (an impressive 100% since 2016), and according to press releases, claims to partner with 60% of technology companies that went public in 2021. In conjunction with an aggressive global expansion strategy, Stripe has expanded its product set along the value chain with the most recent add-ons including card issuing, identification, tax, and revenue recognition.

FIGURE 4: Payments Volumes (2022; in $ bil. equivalent)

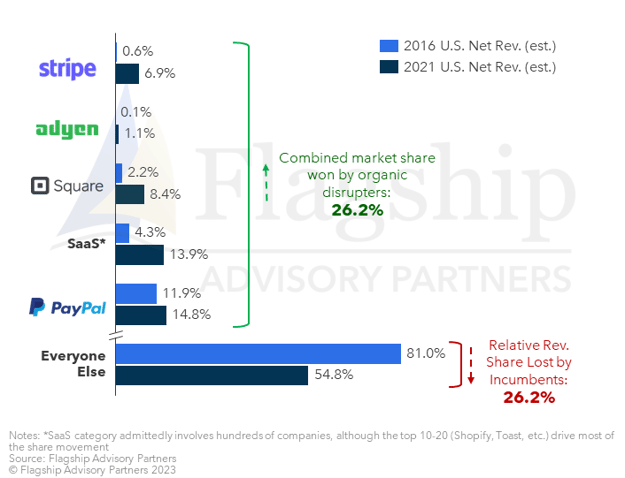

5. M&A No Longer the Key Driver of Consolidation in U.S. Merchant Payments

Finally, our analysis of the dynamics of market consolidation and growth in the U.S. merchant payments market disproved the conventional wisdom stating that M&A is the key driver of consolidation in merchant payments. This is no longer true in the U.S. market. Disparate organic performance led by high-growth disrupters is now the driving force behind U.S. consolidation.

FIGURE 5: Payments Volumes (2022; in $ bil. equivalent)

We look forward to delving into more diverse topics that generate debate and challenge perspectives in the coming year. Should you have any questions, please do not hesitate to contact us at Info@FlagshipAP.com